Самое актуальное и обсуждаемое

Популярное

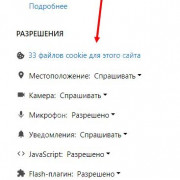

10 расширений для «яндекс.браузера», которые пригодятся каждому

Ubuntu

Теперь рассмотрим процедуру работы с Linux. Если точнее, то с Ubuntu. Это довольно простая и...

98

0

0

10 способов зайти на заблокированный сайт

TOR-браузер - абсолютная безопасность но только для продвинутых?

Очень интересный способ обхода блокировок,...

166

0

0

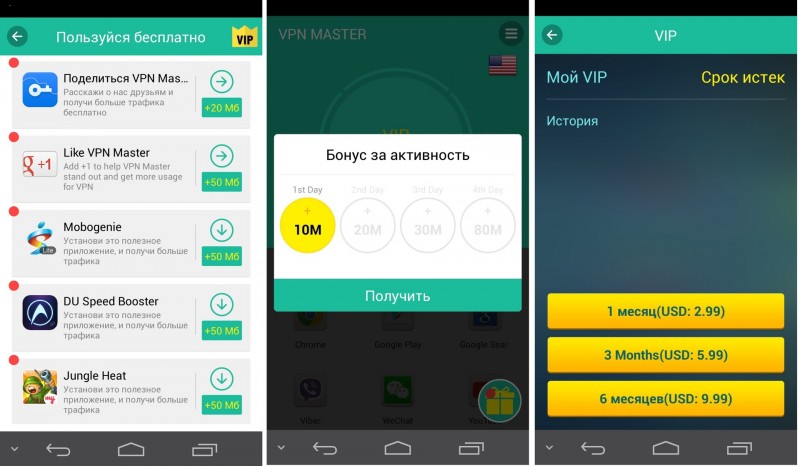

10 лучших бесплатных vpn-сервисов для компьютеров и смартфонов

Описание

VPN Master — Free unblock Proxy VPN & security VPN — свободный и неограниченный, бесплатный...

139

0

0

8 лучших блокировщиков рекламы

Browsers with ad-block

Price: Free (usually)

There are a bunch of browsers with ad-block. These browsers...

125

0

0

20 способов, как скачивать музыку из вк бесплатно на компьютер и телефон

Достоинства и недостатки

Среди плюсов стоит отметить:

бесплатное расширение для любого современного...

573

0

0

8 крутых расширений для новой вкладки chrome

Настройка

Переходим к главному. Как сделать так, что каждый новый сайт загружался в отдельной вкладке?...

85

0

0

42 оператора расширенного поиска google (полный список)

Как отключить подсказки?

Поисковые подсказки – это автоматически сгенерированные системой варианты запросов,...

81

0

0

360 browser 7.5.2.110

Review

360 Browser is a web browser that focuses on the detection and prevention of phishing pages,...

94

0

0

Полезные советы

Важно знать!

3 способа сделать ваш браузер быстрее

Секреты браузера

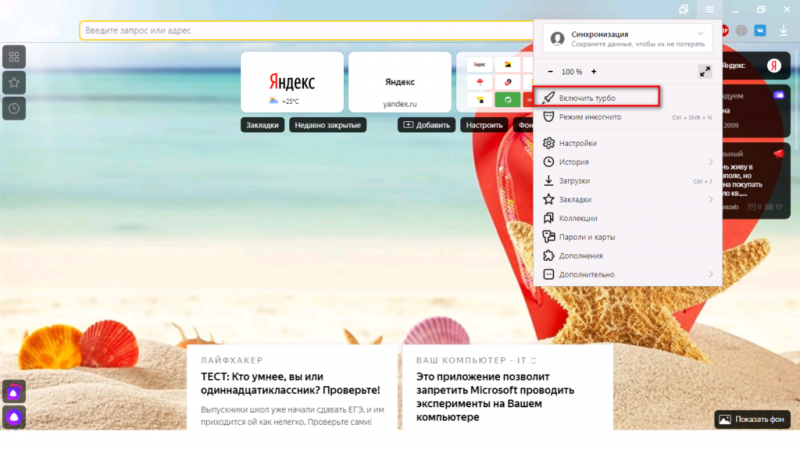

Помимо всего можно «пошаманить» в самом браузере. Давайте посмотрим, что можно сделать для улучшения работы Яндекс.

О том, как ускорить Chrome, рассказано и показано в следующем видео:

Включить...

Читать далее

7 способов узнать, кто и чем занимался на компьютере в ваше отсутствие (+бонус)

11 лучших сервисов для хранения закладок

14 расширений для браузера, которые решат кучу ваших проблем

4 способа добавить закладку в яндекс браузере

360 browser 7.5.2.110 [2014, браузер]

Яндекс.браузер для windows 7 на русском

Скачать google chrome для windows

Как скачать видео с любого сайта через яндекс.браузер

Быстрый браузер для windows 7/10

Рекомендуем

Лучшее

Важно знать!

Как посмотреть историю посещения в яндекс браузере

Как отключить показ истории в браузере

Вне зависимости от того, какое приложение человек использует для выхода в интернет, браузер всегда сохраняет историю. В таком случае каждый владелец Айфона хочет...

Читать далее

Браузер chromium

Криптопро эцп browser plug in

Веб-версия скайп: как осуществить вход

Что такое майл ру агент, зачем он нужен пользователям

Особенности браузера safari

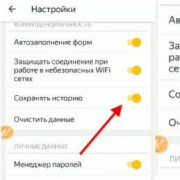

Как очистить историю браузера: пошаговая инструкция

Настройка браузера firefox через about:config

Спутник браузер

Игра войны престолов тактика и стратегия

Новое

Обсуждаемое

Важно знать!

Что такое даркнет? как зайти в darknet с пк и телефона? ссылки на поисковики и сайты

A Chrome-based browser with many surprises

Torch Browser is an alternative web browser that integrates social features, video and audio downloading via streaming and a BitTorrent client.

Based on Google...

Читать далее

Браузер waterfox на русском или как русифицировать waterfox

Скачать алису яндекс на компьютер

Включение tls 1.2 на серверах сайта и удаленных системах сайтаhow to enable tls 1.2 on the site servers and remote site systems

Онлайн игра лига ангелов 2 — легендарная фентезийная браузерка!

Как скачать видео с youtube на компьютер в яндекс.браузере

Как отключить яндекс дзен: простая инструкция

Поисковики даркнета

Браузеры для андроид

Топ-10 программ для скачивания видео с любого сайта

Популярное

Актуальное

Важно знать!

Установить windscribe vpn

Плюсы и минусы

Сервис способен порадовать массой преимуществ и лишь минимальным количеством недостатков. Предлагаем более подробно рассмотреть и те, и другие перед тем как скачать Windscribe VPN.

Плюсы:

малый...

Читать далее

Тег

Не показывает видео в браузере: что делать?

Группа хамелеон

Как восстановить закрытую вкладку в браузере? инструкция для: chrome, opera, mozilla firefox, яндекс.браузер, edge, internet explorer, safari

Как включить микрофон на айфоне

Как войти в вк оффлайн с компьютера

Что такое визуальные закладки для яндекс браузера

Как посмотреть на какие сайты ты заходил?

Установка и переустановка яндекс браузера

Обновления

Статьи

Продвижение в соцсетях: Как привлечь, удержать и вовлечь аудиторию

Статьи

Продвижение в соцсетях: Как привлечь, удержать и вовлечь аудиторию

Эффективное продвижение требует комплексного подхода, включая использование качественных изображений. Когда...

Статьи

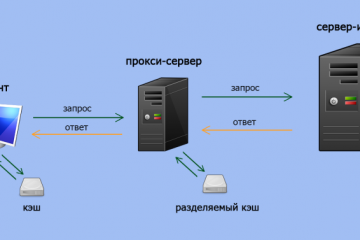

Прокси для безопасности: где и зачем использовать в сети.

Статьи

Прокси для безопасности: где и зачем использовать в сети.

В мире, насыщенном цифровыми взаимодействиями, вопрос безопасности в сети становится более актуальным,...

Статьи

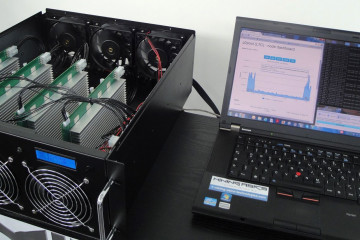

Утройте прибыль: секреты эффективного майнинга криптовалют. Полный гайд для троекратного роста ваших криптоактивов!

Статьи

Утройте прибыль: секреты эффективного майнинга криптовалют. Полный гайд для троекратного роста ваших криптоактивов!

В современном цифровом мире, где технологии криптовалют становятся все более актуальными, обсуждение...

Статьи

Антивирус: Зачем и Как? Онлайн Безопасность в Деталях

Статьи

Антивирус: Зачем и Как? Онлайн Безопасность в Деталях

Защита наших цифровых миров стала неотъемлемой частью современной жизни, и одним из ключевых инструментов...

Статьи

Лицензия ПО: Зачем использовать лицензионное программное обеспечение?

В мире современных компьютерных технологий, когда цифровая сфера нашей жизни становится все более важной,...

Статьи

Обмен криптовалюты: биржи vs. обменники. Выгодные альтернативы.

Статьи

Обмен криптовалюты: биржи vs. обменники. Выгодные альтернативы.

В мире стремительных технологических изменений и финансовых инноваций, криптовалюты стали неотъемлемой...

Статьи

IoT-решения: применение и преимущества в разных сферах! Узнайте больше!

Статьи

IoT-решения: применение и преимущества в разных сферах! Узнайте больше!

Интернет вещей: применения и преимущества IoT решений в различных сферах

В наше современное информационное...

Статьи

Биометрия в банках: безопасность и удобство современных финансовых операций

Статьи

Биометрия в банках: безопасность и удобство современных финансовых операций

Одна из главных проблем - это угроза безопасности данных. Когда данные, содержащие биометрическую...

Статьи

Как восстановить данные с поврежденного жесткого диска HDD

Статьи

Как восстановить данные с поврежденного жесткого диска HDD

Восстановление данных с поврежденного жесткого диска может быть сложным процессом, который зависит...

Статьи

Продвижение телеграм-каналов в 2023 году: тематика, подготовка, методы

Статьи

Продвижение телеграм-каналов в 2023 году: тематика, подготовка, методы

В наше время социальные сети и мессенджеры стали неотъемлемой частью нашей повседневной жизни. В частности,...

Как настроить ленту яндекс дзен под себя?

Как настроить ленту яндекс дзен под себя?

Как отключить Дзен на телефоне

Яндекс.Лончер

Яндекс.Лончер - это главное меню в телефоне от компании...

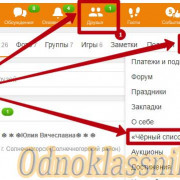

Как быть невидимым во вконтакте

Как быть невидимым во вконтакте

Как пользоваться расширением

Как следить за друзьями

— ели вы хотите следить и получать оповещение,...

Нашли ошибку, неточность или опечатку в тексте?

Выделите её и нажмите Ctrl + Enter

Выделите её и нажмите Ctrl + Enter